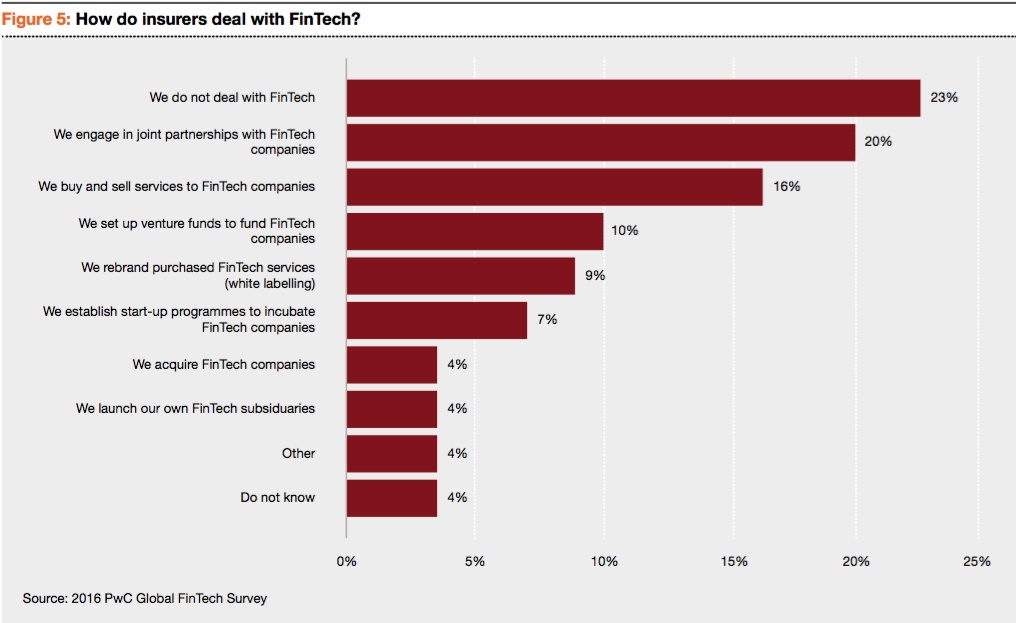

Do insurers get FinTech?

Coming at a time when, according to Gartner, “half of CEOs expect their industries to be substantially or unrecognizably transformed by digital”, the apparent lack of engagement with FinTech displayed by insurers in a recent PwC US report makes for some perplexing reading:

While only 23% “do not deal with FinTech”, 4% admit they “do not know” how to deal with it, and the rest are all taking very different (and predictable) approaches, ranging from trading and partnering with FinTech companies, to investing, incubating and even acquiring them.

It is tempting to simply dismiss all this as market immaturity, or blame these limited, fragmented responses on being too busy with core business activities. After all, with so much FinTech-driven disruption already occurring in the wider financial services sector, it was only a matter of time before insurance companies would start to feel some of the same tremors. In fact, the potentially existential threat posed by digital to business as usual has been on the C-suite’s radar for a few years now – to the point that CEOs are now taking charge of digital transformation personally and with renewed urgency because, as Aviva’s Mark Wilson recently put it, “insurance is in the Stone Age, while other people are circling Mars”.

It doesn’t get much more ‘core business’ than when the CEO steps into the ring, so what is stopping most insurers from seizing what PwC are calling a “golden opportunity to innovate“?

Complexity and competing priorities

In common with the wider financial services sector, insurance is facing many of the same systemic pressures, demanding that insurers find more responsive ways to deal with shifting customer demographics, higher service expectations, low levels of customer trust and satisfaction, the re-organisation (and growing complexity) of distribution channels, and widening regulation demanding greater transparency, to name a few.

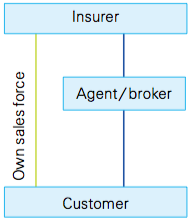

There are other similarities: the insurance industry’s dependency on brokers to sell their products, and the associated reluctance to upset these important channels by going to customers direct (there are notable exceptions, such as UK car insurance in the UK, where direct sales via telephone, web and price comparison sites account for about 2/3 of all sales) also echoes the wealth & asset management sector’s dependency on intermediaries, meaning that innovation in some product areas is more likely to emerge from the distribution chain than the insurers themselves.

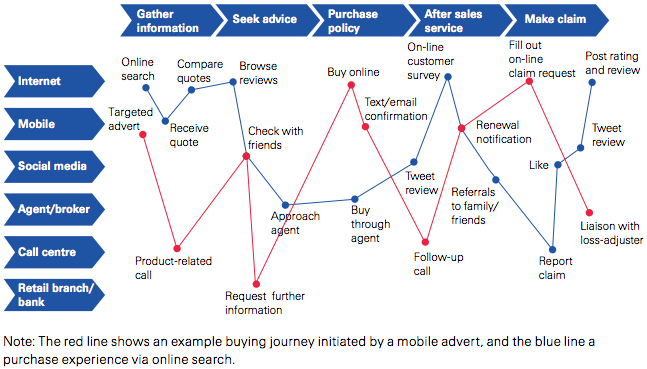

Much of the insurance industry’s work on digital to date has focussed on a renewed interest on customer experience (CX in the jargon), partly because customer acquisition and retention are key to business success, but more specifically because the convergence of digital, social and mobile channels have made a previously simple distribution picture become quite fragmented and confusing for the traditionally offline majority of industry players.

According to an excellent Swiss Re report (Digital distribution in insurance), the distribution journey has gone from this:

to this:

… in the space of less than a decade. This level of fragmentation – and customer choice – is only going to continue, because each of these areas of customer interaction offer significant opportunities for FinTech entrants, who – in line with their counterparts in other financial services areas – will zero in on the weakest links of the value chain and pursue these with relentless focus.

The current obsession with the customer journey and ‘CX’ is therefore understandable, but even if insurers were to get this piece of the puzzle absolutely right, it would only scratch the surface of the wider digital transformation challenge facing the industry.

>You may also be interested to read our research report on The Barriers to Digital Transformation which includes our latest thinking on organisational structures and agile attributes.

Lack of credible digital competition

For all the ‘startups eating the world’ bluster, entering the insurance industry is not very easy and can be very expensive. As Balderton partner Rob Moffatt points out in his insightful Medium post, the main barriers are: regulation, requiring new entrants to become proficient in navigating the marketplace and its many regulatory sandbanks; financial clout, because responsive design WordPress templates are not enough when an insurance startup has to pay out on the inevitable claims; and access to closely-guarded (and often poorly digitised) industry data, without which underwriting is unlikely to be accurate – even with predictive analytics, it would take several years to create an accurate risk pricing model.

For all these reasons, FinTech innovators would be better off partnering with incumbents who can provide all of the above, and enhancing or extending their business models to mutual benefit, rather than try to disrupt them completely at a prohibitive cost. Again there are well-funded exceptions here, such as health insurance startup Oscar (which has raised $3/4bn but is yet to make a profit).

As for the ubiquitous FinServ fear of the slumbering tech giants awakening (with lots of cash, customer data, and immense reach), Moffatt thinks the danger is over-baked, as in reality insurance is “too hard and too boring” for the industry’s best developers to prioritise over more exciting developments.

Combined, these factors have lulled insurers into a temporary sense of security, thus allowing the innovation can to be kicked a bit further down the road. While this may hold true of the challenge posed by startups, insurers cannot afford to sit on their laurels while the industry’s central tenet – the ability to properly price risk – is itself coming under severe pressure from a combination of fast advances in technology and wider industry mega-trends, which are challenging the industry’s established underwriting models.

Emergence of new risks

Just as startups find it hard to enter a big hairy market like insurance, so the established industry participants struggle with a raft of new and hard-to-predict risks, which are becoming a feature of delivering financial services in a VUCA world.

The first and most obvious one is, of course, the volatility of current (and foreseeable) investment market conditions. Pension funds and insurance companies have been deeply intertwined in both the equities and corporate bond markets since the 1980s, when deregulation and buoyant markets attracted huge amounts of funds searching for aggressive returns. To all intents and purposes, insurers and pension funds drove the development of the stock market as we know it today.

However, the current ZIRP (and increasingly NIRP) return environment has led to massive – and largely unsustainable – gaps in defined benefits exposure, as evidenced recently by the Universities Superannuation Scheme’s (USS) decision to cut expected pensions by 25%, and the current debacle over claims that Philip Green’s Arcadia might be responsible for plugging another very large gap in BHS’s pension fund.

These are not issues that digital innovation can directly address, but they do contribute to a generational movement away from established insurers and financial services companies at large, and towards smaller, friendlier, more collectivist alternatives, such as peer-to-peer insurance, which are beginning to spring up in no small part as a result of these ongoing issues.

Geography is also increasingly playing a role in shaping the insurance industry. Outside of the traditional US and European markets, SE Asia’s burgeoning middle class is already providing the main engine for future growth, while simultaneously its tech-savvy demographics are challenging the industry to develop more innovative connected solutions.

But there are other issues keeping insurers up at night, and in each case they emerge from both the known and evolving risk types that the industry is trying to mitigate, such as the effects of climate change, an ageing population, and underinsurance, to name a few.

There are plenty of opportunities offered by digital innovation applied to actuarial science (mainly around big data modelling, predictive analytics, machine learning and AI), but despite the arrival of clever startups like MeteoProtect, Atidot, AnalyzeRe, and QuanTemplate, it is still very early days.

There are also new and emerging risks to contend with, which are a direct effect of technological progress, and for which little or no historical risk data is available. The industry is just coming to grips with the risks posed by cybersecurity breaches, but how do you underwrite the risks posed by autonomous vehicles, drones, and evolving AI-driven robots? Virtually none of these can be sensibly underwritten by reference to historical risk data.

However, taken as a whole, we can begin to see a not-too-distant future where risk pricing is dictated not only by better mining of insurers’ info treasure troves (including perhaps the monetisation of dark data), but also by big data propositions bringing together AI and predictive analytics with profiling and personalisation. This combination of both historical and future probability data capabilities is what, in my view, will dictate the insurance industry’s winners and losers over the next decade.

Industry modernisation: the final frontier?

The insurance industry is undergoing momentous change with no simple one-size-fits-all prescription, but given the complexity of some of these challenges there is a growing imperative towards investing in innovation and industry-wide collaboration in an attempt to solve common problems.

Several firms are already experimenting with new business models and more digital ways of working, such as Aviva’s Digital Garage, AXA’s recent commitment to digital transformation (backed by its own Strategic Ventures fund, InsurTech incubator and internal innovation platform Start-in), as well as other firms’ more tentative entry into the space through sponsorship of third-party incubators such as Startup Bootcamp InsurTech.

But much of this incubation and innovation work is focussed on developing new products, experimenting with new services, and improving CX to maximise transactions – i.e. most of this effort is business as usual by different means, and it is tied to an increasingly discredited ‘be like a startup’ thinking. Startups and corporations are very different, and for good reason. To quote Steve Blank: “A startup is a temporary organisation in search of a repeatable, scalable business model… A corporation, by contrast, is a permanent organisation designed to execute a repeatable, scalable business model”.

Insurers have already found a repeatable and scalable business model – insuring risk – which simply needs to be brought up to date in the face of multiple challenges and constant tech-driven change. While playing startups is good for PR and might occasionally yield a return, it is not going to solve the industry’s innate inability to innovate from within, which is what needs to happen.

So what is stopping insurers from reinventing themselves? Predictably, some of the biggest challenges faced by companies in this sector are internal:

- Insurance is trying to pull itself out of legacy systems, many of which were originally custom-built to manage what are now commodity transactions;

- The hierarchical nature of the sector’s corporate structures and the inherent conservatism of the industry’s corporate managers (which lies in stark contrast to the risk-taking entrepreneurial values which have always been a feature of the industry, from Lloyd’s Coffee House onwards);

- Industry-wide lack of internal digital literacy, skills and knowledge;

- Related HR, employment and digital talent attraction and retention issues.

So in addition to managing wider industry issues, there is an urgent need for insurance companies to develop the human competencies required to organically ‘sense and respond’ to constant change, and learn how to be more agile without losing sight of their existing experience, clout and marketshare, as a much more viable alternative to innovation tourism or big-bang, top-down ‘change management’ programmes. In other words, insurers need to reform and reinvent themselves by undertaking a process of sustainable, long-term transformation, with digital skills at its core, leading to greater resilience and responsiveness to change.

If you want to find out more about how to kick off a meaningful digital transformation process inside your Financial Services organisation, please head over to our dedicated pages, or just get in touch to discuss.

>If you’d like to receive our weekly newsletter which shares our latest thinking each Thursday along with a round up of interesting links, you can sign up here.