He began by asking where future productivity gains and jobs will come from, given that we appear to be in a jobless recovery, with no return to previous levels of employment some 70+ months since the beginning of this recession, compared to the 6-15 month lag that we saw in the C20th. Without productivity gains and job creation, obviously we cannot sustain the same quality of life and public services we are used to.

The core of his thesis is that there are three broad types of innovation, and they combine to form a cycle of invention, improvement and optimisation that produces free capital to begin the cycle of innovation once again; but what we are seeing today is that cycle is broken and cash is being hoarded at the expense of value-creation.

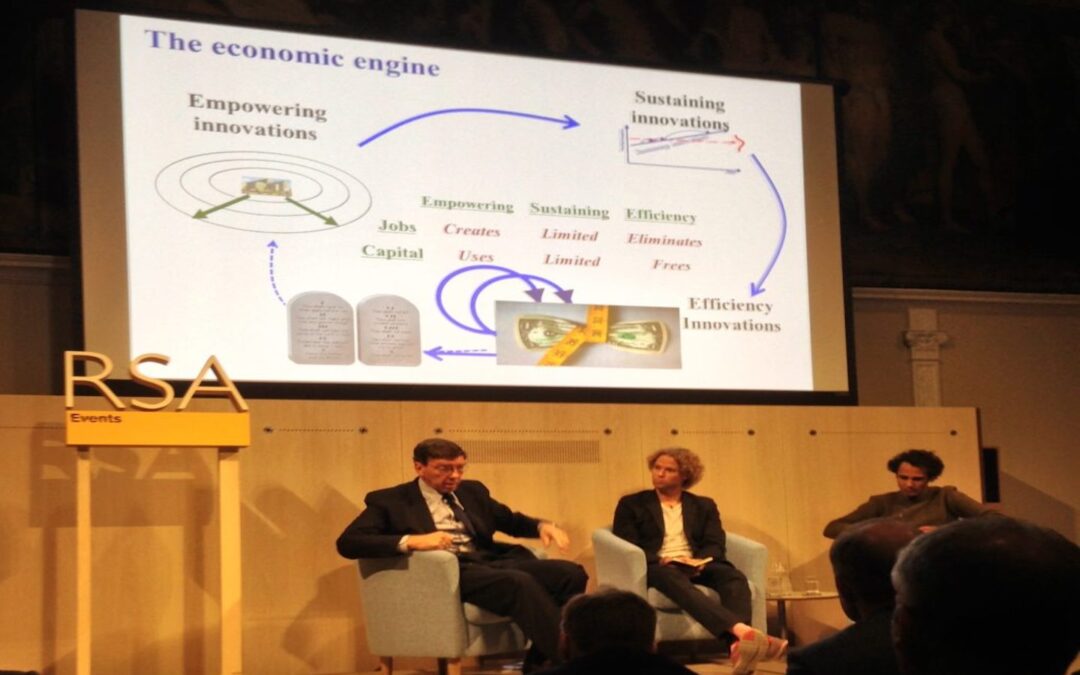

The three types of innovation he talked about are:

- Empowering innovation. This turns expensive products and services into cheaper, more accessible items, thereby making innovations available to more people. A good example is the innovation that saw mainframe computers supplanted by personal computers, and later by smartphones. Most jobs in the economy are created by empowering innovation. This process consumes capital but creates jobs.

- Sustaining innovation. This makes good products better. It creates few jobs and needs only limited capital. In a sense, it is part of a zero sum game since people will buy the new improved product, but not the old one, which is replaced. This process requires limited capital and creates a few jobs.

- Efficiency innovation. This allows you to make the same product at lower prices to sell to the same people. It is largely about optimisation and cost reduction. Walmart and the insurance industry are two examples that people are familiar with. These innovations tend to eliminate jobs and free up capital.

At the end of this loop, in an ideal world, the capital freed up by efficiency innovation fuels a new cycle of empowering innovation. But the problem is that business is now so in thrall to finance, that capital accumulation is their primary goal, rather than value creation through innovation, which is by its very nature risky. The cycle is broken, with serious implications for future productivity gains and employment.

Clay went on to say that, in his view, the development of the spreadsheet has changed the practice of management more than anything other tool. Calculating IRR and ROIC/ROCE are so easy that they have become the only way that the MBA generation are taught to manage a business these days. Management has become a simple task of optimising numbers to maximise short-term shareholder returns, and the finance profession has achieved pre-eminence over leadership and management theory.

He refers to Gilders Axiom for inputs, which says that among the inputs required to create an output, the scarce, costly resources require husbandry and should be deployed only where they produce the best returns. Modern finance began with the idea that capital was just such a scarce resource, and so should be deployed only where it could achieve maximum returns; but that is no longer the case and we now have an abundance of capital seeking fewer high return investment opportunities (which is itself partly a result of finance’s preference for incremental efficiency innovation over potentially higher-return empowering innovation).

Also, Clay pointed out, finance is largely about ratios. ROIC, ROCE, etc., are ratios that can be improved either by adding to the top line or cutting from the bottom, and it is always easier to cut costs than to create value, which explains why so much CFO activity is aimed at the former, not the latter. If you invest in empowering innovation, the returns could be huge but they occur over the long-term, whereas efficiency drives are able to generate capital very quickly. As a result of this domination of business by finance theory, Clay estimated the level of empowering innovation in the United States has fallen to around 30% of its previous level over the past two decades. We are now awash in capital but cannot create jobs or innovation. He cites Japan as an example of where we are headed as a result, where extraordinary levels of invention and innovation from the 1960’s onwards gave way to business school thinking, resulting in a flat-lining economy and a cost of capital that is close to zero. No amount of Quantitative Easing can reverse this trend.

Corporate balance sheets have never looked better, and many companies claim they are gearing up to invest, but they rarely do. Even in R&D, only a minority of activity is aimed at value-creating empowering innovation. Whilst large firms often struggle to do empowering innovation because the new markets this creates are often too small in the early stages, Clay suggests the answer to this lies in creating spin-off units, as IBM did to create the PC whilst the firm was still focused on mainframes, as this gives them the ability to seed the future without betting the farm.

So how do we stimulate more empowering innovation? One way, as always, is through state-funded (often military-related) initiatives such as DARPA, NASA, etc. Another way suggested by Clay might be variable tax rates based on how long capital is invested, perhaps hitting negative rates when capital is invested for long enough in pursuit of invention or real innovation.

Whilst these may help, personally I think the fundamental problem outlined by Clayton Christensen goes much deeper, into the behaviours and motivation of individuals within the world of finance. For much of our history, capital accumulation was not the sole goal of business-people. Like everyone else, they lived in communities and societies that made the pursuit of status and respect just as important as cash, and finance was a service to business, not the other way around. Economies were largely national, and in times of need, those with money might be expected to help out for the good of the nation. These days, pure capitalists (i.e. people who move money around to multiply its value, not those who build businesses and create shared value) are global, mobile and in many ways separate from the people around them – even the states in which they live. National economies can no longer regulate capital, and we have seen since 2007 just how untouchable the finance industry has become, despite its role in the banking crisis. As Gillian Tett points out in the FT today, the Bank of England estimates that 40% of the benefit from Quantitative Easing has gone to the top 5%, including of course the bankers, whilst the dangerous world of shadow banking that was implicated in the crash has increased by over 13% to $67tn since 2008. Every incentive currently operating on the behaviour of financiers acts in favour of speculation, or at best incremental efficiency innovation, and against value-creating empowering innovation. How can we change this?

The technology sector is built on innovation, and so offers us some hope. But for as long as the goal of highly successful technology firms such as Facebook and Twitter is to go for IPO – i.e. to become a financially tradeable product – rather than to build sustainable businesses that will be around 100 years from now, perhaps we have to look towards the smaller makers and innovators for the kind of empowering innovation that Clay talks about.