We often hear about how overheated the London tech startup sector has become and how little real innovation is actually occurring, when so many startups are essentially media or e-commerce companies using social tech of one kind or another to deliver old services on new platforms.

By contrast, the London financial technology (FinTech) sector is one area where startups are demonstrably generating new ideas, new IP and new business models, which are posing a seriously disruptive challenge to many established financial services (FinServ) companies.

Just how much of a challenge the rise of innovative FinTech is already posing to traditional FinServ was very much in evidence at the recent Innovate Finance Big Data event, hosted by Level39, which provided an opportunity to examine the FinTech innovators shaping the market and the challenges that are holding back the creation of this multibillion-pound industry.

Punctuated by keynotes from Google’s Head of Innovation Yuval Dvir and Lloyds Bank’s Gary Sanders, among others, the event also provided an opportunity for Innovate Finance’s outgoing CEO Claire Cockerton to introduce her ‘geek capitalist’ successor, Lawrence Wintermeyer, after doing a great job of building the Innovate Finance community and establishing it firmly as a key part of London’s startup scene.

The energy, drive and sense of mission displayed by the founders at this event stood in sharp contrast to the soul searching and occasional M&A plans of the traditional FinServ companies present. “Destiny”, one founder suggested grandly, “is on FinTech’s side” – and the sector’s spectacular growth in a very short time seems to bear this out.

Although the majority of FinTech startups have, thus far, only focussed on plucking the low-hanging fruit offered by FinServ’s spectacularly poor customer service and over-intermediated value chains, this alone has already led to strong growth, estimated by Russ Shaw to be worth “£20b to the UK annually, and employ[ing] over 44,000 in the sector in London alone – more than both in Silicon Valley and New York”.

Or, as the Economist put it recently:

“From payments to wealth management, from peer-to-peer lending to crowdfunding, a new generation of startups is taking aim at the heart of the industry – and a pot of revenues that Goldman Sachs estimates is worth $4.7 trillion [globally]”.

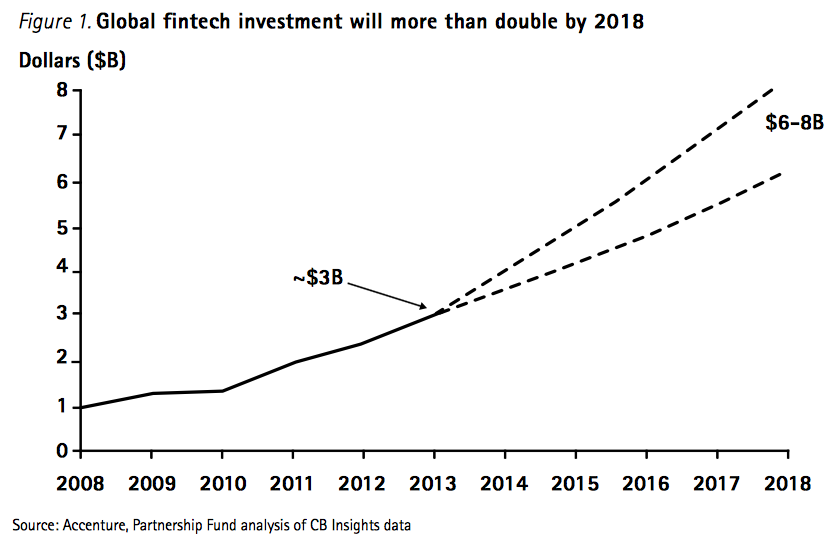

This, in turn, is attracting fast-increasing levels of investment globally, “driven by new digital technology, regulations, consumer behavior and the need to reduce costs”, which Accenture estimates will grow from the current $3 billion to $6-8 billion by 2018:

All of this activity is already having an impact on FinServ’s market position and this is forcing established companies, mainly banks, to take stock and formulate a response. Key traditional revenue-generating areas have already come under attack and FinServ is losing increasing amounts of revenue and profits to new businesses entering the market – many of which are FinTech startups.

For example, US banks earned about $150 billion from lending operations in 2014, but Goldman Sachs (as reported by Bloomberg recently) now estimates that

“$11 billion plus, or 7 percent of annual profit, could be at risk from new sources of credit over the next five-plus years”. To be clear, this is not just about loss of profits, because “emerging players will force the incumbents to change competitive behavior… We would expect pricing of products to adjust, driving potentially lower returns.”

Remember, this is only lending. In fact, FinTech has been targeting the weakest links in the value chain of other core banking services – payment processing, FX, investment management – as well as addressing customer service issues, which will inevitably take new business away from the established players.

Whether or not FinServ can credibly continue to attract new business without changing its business model or finding new ways of engaging with customers will partly depend on whether established companies can offer relevant digital services, presence and engagement with millennials, as Joe Polverari of cloud-based financial platform Yodlee recently argued:

“This generation of digital natives is about to move into its prime spending years and exhibit fundamentally different financial behaviors than the generations before them. [..] They also hold very different attitudes about banking and credit. Big banks represent 4 of the 10 least-loved brands by millennials, according to the Millennial Disruption Index, and one in three believe that they won’t need a bank at all in a few years […] 63 percent of American millennials have no credit cards, nor do they seem to want them. Old approaches to financial services will not hold up for long.”

Being able to provide relevant services to this powerhouse generation – while also continuing to appeal to baby boomers, who have the spending and investment power now and are also the second largest group online – will be one of FinServ’s defining challenges in the coming years.

Meanwhile, startups like recently-acquired LearnVest (originally a financial planning service for women, but now connecting both women and men with human financial advisers) and WealthStorm (an online investment platform which managed to win $1bn in assets under management in less than three years just by focussing on wealthy millennials) are among those reaping the benefits in the US, while UK companies like Monitise (the world’s first mobile banking, payments and commerce ecosystem) and startup Monese (which lets you open a bank account in minutes on your mobile, still in beta) are also benefitting from this shift.

All this digital and social business activity is disruptive enough, but the challenges posed by specialist startups, FinTech accelerators and consumer brands pale into near-insignificance if cash-rich tech companies enter the field in a big way.

Unlikely? In Q3 2013, Tianhong Asset Management Co. was acquired by Alipay (Alibaba’s PayPal equivalent in the massive Chinese market), leading to the establishment of the Yu’E Bao money market fund, which allows Alipay’s customers to invest their spare cash online. As of June 2014, Yu’E Bao had recorded AUM inflows of around $87bn – in less than one year.

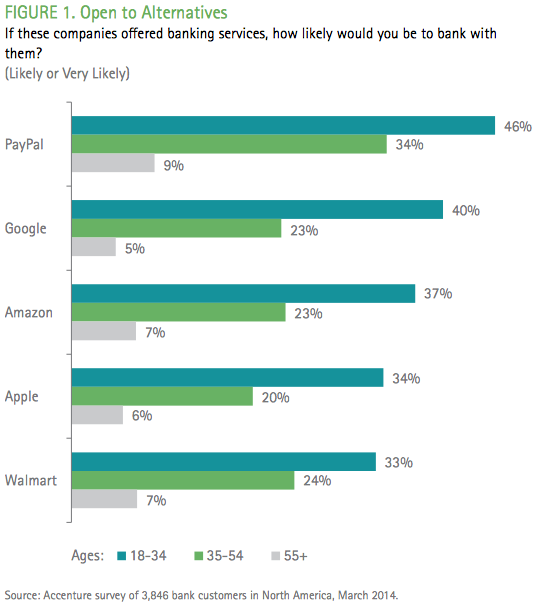

So, if we turn our attention to those tech companies, like Google, Apple, Amazon, and Facebook, whose cash reserves are greater than those of many countries, and whose deep, intimate knowledge of their customers’ behaviour is unmatched, we can easily imagine a future where the FinServ industry could be changed forever. In a 2014 Accenture survey, a number of US banking customers clearly stated their willingness to bank with these tech giants, as well as other non-bank brands:

How is the FinServ industry responding to this clear and present danger? Rather than working to imagine how the industry can reinvent itself in the face of so many converging pressures, such as loss of trust, heightened customer expectations, regulatory pressures, lower margins and market volatility, many FinServ companies’ response ranges from blissful ignorance to distracted attention.

There are some notable exceptions, of course, such as UBS’s blockchain research lab in London, which is working to “experiment with how […] the underlying technology behind bitcoin can be adapted to process a wide range of financial transactions in a more efficient and cost-effective way and active engagement”, but overall FinServ’s engagement with FinTech’s threat has been slow and lumbering.

This may seem an unfair indictment. After all, it was only recently that the likes of Jamie Dimon warned JPMorganChase’s shareholders

“Silicon Valley is coming. There are hundreds of startups with a lot of brains and money working on various alternatives to traditional banking. […] They are very good at reducing the ‘pain points’ in that they can make loans in minutes, which might take banks weeks.”

In fact, this is not new at all. Warnings were sounded as early as 1994 by no less an investors’ darling than Bill Gates, whose prediction that “We need banking but we don’t need banks anymore”, and his labelling of banks as “dinosaurs”, caused some media attention but went largely unheeded by the FinServ industry as a whole (admittedly, Microsoft was pinning its banking hopes on the failed Intuit acquisition at the time, but the essence of Mr. Gates’ prediction has largely come true and, ironically, Intuit is currently one of the biggest buyers of FinTech on the market).

This is surprising, given the resources available to the FinServ, its research capabilities, its armies of analysts and the billions spent each year on external advice. So what is going on? Why has it taken so long for the sector to start paying attention? No one answer fits all, but several factors have contributed to this situation. A lot of the early attention that FinServ did pay to the coming sea change only went as far as getting its basic, online, transactional house in order.

Much of this happened in the 1990s at the hands of ‘interactive agencies’, many of which disappeared with the dotcom earthquake that buried both their hubris and the fragility of their ‘bricks and clicks’ business thinking. The current online presence of some FinServ companies still suffers from the same unimaginative advice which large consultancies, and system integrators continue to dispense to FinServ courtesy of hard-to-cancel framework contracts. However, poor usability and boring UX, prevalent as they are in FinServ, are not the whole explanation.

Some point to the industry’s inherent conservatism and unenlightened leadership – i.e., what seems obvious, run-of-the-mill to millennials and FinTech startups is still largely unheard of in some boardrooms focussed on just making money – but perhaps there is a different, more nuanced interpretation of this ‘business as usual’ inertia.

At the heart of FinServ’s struggle to adapt is what Clay Christensen’s calls the Capitalist’s Dilemma – in essence, the thesis is that there are three broad types of innovation, which combine to form a virtuous cycle of invention, improvement and optimisation that produces free capital to begin the cycle of innovation once again; but what we are seeing today is that the cycle is broken and cash is being hoarded for short-term reasons at the expense of value-creation (you can read more about all this in our post on this topic here).

In other words, just as many US computer hardware companies were unable to keep innovating while they were so busy shifting computers globally, and just as energy companies have struggled to respond to the existential threat of oil depletion while still busy pumping and selling billions of barrels of crude, so FinServ has been under so much market and shareholder pressure to post short-term growth that anything else looks like a distraction – although we may be reaching the beginning of the end, which is a really good time to rethink your business model.

So the question is, how can FinServ companies better adapt to the present and prepare for the future?

The first reality check is that, even accounting for no changes, FinServ’s sheer size means that it would take several years of concerted FinTech competitive activity to replace the market power of the incumbents, but in reality, for all its apparent lack of urgency, FinServ has a long history of survival and re-invention when the penny finally drops.

In addition, FinServ’s cash reserves and investment capabilities mean that it might well be possible for companies to spend their way out of the challenge – after all, the main exit route for most FinTech startups is precisely to be acquired by the giants they challenge. One problem with this approach is that large companies (FinServ or otherwise) have a terrible record seeing M&As through successfully, a topic that we have covered at length elsewhere on this blog, and so it is likely that the innovative IP acquired in this way could die with the startup that spawned it, once the founders have left for better climes with a wad of cash.

A more resilient, long-term approach – one that can foster, rather than kill, innovation – might be for FinServ to better engage with FinTech and position itself to reap the rewards of the ‘outboard brain’ provided by the tens of thousands of young, motivated, intelligent, passionate people building their businesses and dreaming of greatness. Sponsoring FinTech incubators, building home-grown FinTech accelerators, supporting innovation labs, building partnerships, and providing ongoing investment (in addition to direct investments, we are beginning to see banks launching FinTech VC funds of their own) are all part of FinServ’s survival toolkit, as is its historically masterful ability to create revolving doors between seemingly competitive sectors, to mutual benefit.

This activity is happening right now, but it should not be cause for complacency. FinServ companies need to reform internally to be able to better handle the volatile, uncertain, complex and ambiguous (VUCA) business conditions under which they must now operate – of which the FinTech revolution, in particular, is only one element. How can FinServ companies go beyond simply reacting to external factors, towards the creation of a human-centred, resilient, customer-first sector? Or, as Alistair Crane of Monitise puts it,

“There’s a wealth of opportunity to transform how banks serve their customers, and develop whole new streams of revenue. The possibilities are limitless, but this is where the paved road runs out and you have to start making your own way – and success and survival will depend on banks having creativity and boldness. It depends, more than anything, on having a ‘human first’ mindset that has been largely absent from traditional banking vocabulary.”

We believe that FinServ companies need to addresses the strategic need to modernise internally, putting in place strategic efforts to address the internal capacity, staff learning and development, organisational design, culture change, and service integration capabilities required to survive and thrive in an era of constant tech-driven change.

‘Digital’ is no longer just the domain of marketing agencies and it is not enough to just sponsor a start-up incubator and hope for the best – digital transformation is now a C-suite strategic issue, which requires FinServ companies to develop new skills, improve knowledge and build the right capabilities to survive and thrive in the ‘new normal’. But how?

Our experience of delivering cutting-edge social business, digital capacity and social technology projects for leading financial services firms – together with our ongoing startup incubation and process innovation work – suggests that, in order to succeed, firms must go beyond the current focus on campaign-based social marketing and trying to move old business models onto new platforms.

There is no one-size-fits-all strategy for getting this right, but working with our FinServ clients has taught us that focussing on the organisational capabilities needed to successfully engage with digital transformation, and taking an iterative approach to developing these is often the right starting point because, given the speed at which FinTech and other threats move, the overall future operating model is usually not 100% clear at the outset.

One possible approach is our QuantOrg™ methodology, which has been developed precisely to help traditional firms to plan, execute and measure the right steps to achieving sustainable digital transformation. Enabling firms to position themselves at the centre of an interconnected digital and social ecosystem will allow them to take advantage of the many digital opportunities to engage with their end-customers, channel partners and employees, while also building long-term capabilities and better resilience to constant change.

We have become very excited by the opportunity to support FinServ firms navigate this rapidly-shifting landscape, which is why today we are launching our dedicated service offering, tailored to the specific needs of this sector. Over the next few weeks, we will also publish several additional blog posts covering some of challenges and opportunities emerging in FinServ and FinTech in greater detail.

Watch this space, as they say – and please get in touch if you’d like to discuss any of these topics.